In March 2026, Hanahana Beauty exited 500 Ulta Beauty locations and told its customers to buy directly. The announcement came via TikTok - the same platform fueling a dupe economy that makes premium positioning harder to justify by the day. That collision sits at the center of beauty dupe strategy in 2026: the industry's most powerful distribution channel and its most destabilizing competitive force are the same app.

What the discourse around dupes keeps missing is the consumer it is actually describing. The data does not support a clean story of premiumization under siege - it supports something more complicated, and more strategically useful, for any brand willing to read it clearly.

How the Dupe Economy Is Actually Reshaping Beauty Brand Strategy

The Dupe Buyer and the Premium Spender Are the Same Person

The beauty industry has been treating dupe buyers and premium spenders as separate segments. The data says otherwise.

According to a March 2026 First Insight study of 2,151 consumers, 59% of Gen Z actively trades down on household staples - food, beverages, everyday essentials - to fund premium purchases in health, wellness, and beauty. Skincare and beauty ranked as the second most common destination for that redirected spending, with 22% of Gen Z willing to pay a premium in the category. This is a consumer who has made a deliberate, funded decision that beauty is worth spending on.

The same study found that quality - not price - is the top purchase driver for beauty and skincare among Gen Z, cited by 33% of respondents. In food and beverage categories, price is the top driver. In beauty, it is not. The consumer navigating the dupe economy has not abandoned the idea of paying for quality. She has raised the bar for when a brand earns it.

That distinction changes the strategic question entirely. A brand that reads dupe buying as price-chasing will respond with promotions and price defense. A brand that reads it as quality-testing will respond with proof - ingredient transparency, efficacy claims that survive scrutiny, community that validates rather than markets. Those are different budget decisions, and only one of them addresses the actual behavior.

The Retail Exit That Explains the Real Margin Problem

Hanahana Beauty's Ulta exit is the clearest recent illustration of what dupe-market economics are actually doing to mid-tier beauty brands - not at the revenue line, but at the cost structure underneath it.

Founder Abena Boamah-Acheampong, told Beauty Independent after the March 2026 exit, describing what retail actually requires: at minimum $1 million in working capital to enter, significantly more to sustain a meaningful footprint. That capital, once deployed into slotting fees, field representatives, and minimum order quantities, competes directly with the budget a brand needs to defend its positioning against dupe challengers. A brand spending everything on shelf presence has nothing left for the differentiation work that gives a consumer a reason to pay the premium in the first place.

The deeper problem Boamah-Acheampong named is customer intelligence - or its absence. "When you're in so many different stores, quality control is very different than when you're direct-to-consumer," she told Beauty Independent. "We know who our audience is. We own the customer. When you're in retail, you see the numbers, but you don't know who they are."

In a dupe-saturated market, that loss of customer intelligence is structural vulnerability. Dupe culture is specifically designed to interrogate brand claims through peer comparison. The brand that does not know its customer cannot make the case to that customer - and the customer, armed with TikTok comparisons and peer review, will run the test herself.

Hanahana's pivot to DTC is not a retreat. It is a bet that customer data is worth more than distribution scale - and that the brand that knows its buyer is better positioned to survive a dupe challenge than the brand with 500 doors and no direct relationship.

The Threat Behind the Dupe Threat

Dupe culture has a counter-movement, and it is growing on the same platform.

A de-influencing trend has emerged on TikTok — documented by Her Campus — in which creators specifically coach consumers to question whether any product is worth the premium, sharing lists of purchases that failed to deliver on their claims and actively discouraging followers from repeating the mistake. The target is brand-controlled marketing narratives, and beauty is the most exposed category: emotional premium claims like "transformative," "clinical-grade," and "luxury" are exactly the claims most vulnerable to peer deflation.

De-influencing compounds the dupe threat in a specific way. Dupes attack the price premium. De-influencing attacks the trust premium. A brand facing both simultaneously has lost the two mechanisms that justify charging more than the drugstore alternative.

The trust data makes this concrete. According to a March 2026 study by Walr on behalf of We Are Talker, surveying 2,000 US Gen Z consumers, customer reviews were the most trusted information source for 72% of respondents when deciding whether to engage with a brand. Influencer content ranked seventh at 55% — below independent research, expert opinion, news coverage, brand advertising, and brand social media.

A beauty brand investing in influencer partnerships to counter dupe culture is spending on the channel that ranks last among the sources its target consumer actually trusts. That is not a content problem. It is a structural trust deficit — and paid creator spend does not close it.

The Strategic Question - and What the Data Actually Says

Three forces are in active collision in the US beauty market right now.

Gen Z has made beauty a genuine spending priority — funded by cuts elsewhere, driven by quality standards, not price sensitivity alone. The dupe economy has given that consumer a calibration tool: a mechanism to test whether the premium brand's claim to superior results is real or manufactured. And de-influencing has eroded the channel brands have most relied on to make that case, while elevating peer review as the dominant trust signal.

In that environment, the conventional beauty brand response — invest in influencer partnerships, defend retail shelf presence, protect the hero SKU — is also the expensive one. And expensive strategies require that your assumptions about the consumer are correct.

Standard Insights surveyed 576 US adults — nationally representative — to find out whether those assumptions hold. We put 15 handpicked brands in front of them, spanning legacy giants like L'Oréal Paris and Estée Lauder, established challengers from Rare Beauty to ILIA Beauty, and lean disruptors built on the premise that transparency beats heritage. The central question: are dupe buyers permanent defectors, or a trial segment that converts if the premium brand gives them a reason?

The data resolves it. The prestige beauty contract has not softened. It has been structurally renegotiated — and the terms are worse than most brands think.

The Survey Verdict: Three Numbers That Change the Calculation

55% of all respondents cite price-to-quality mismatch as their primary frustration with established beauty brands. Not a minority grievance — a majority position held across income levels, age groups, and purchase frequencies.

47% of all respondents have already replaced at least one premium product with a cheaper alternative found online or on social media. Among active buyers specifically, that figure climbs to 61%. Active trade-down is the single most common spending behavior in this category — practiced overwhelmingly by the consumers most engaged with it.

And when told that a $12 drugstore moisturizer shares 80% of active ingredients with a $65 prestige equivalent, 50% say they would switch to the cheaper option immediately. Only 10% would maintain the premium purchase on brand experience and packaging alone.

That last number is the verdict. The emotional premium — the portion of prestige pricing that is not about formula — retains just one in ten consumers when ingredient parity is introduced as the decision criterion. Heritage, packaging, sensory experience: together they hold a narrow slice of the market. The rest is making a calculation, and the calculation is increasingly not running in prestige beauty's favor.

The full dataset — including brand-level scores across all six dimensions, segment breakdowns by age, income, and buyer status, and the five consumer personas — is available in the interactive report. Access the full report — free →

The Brand Battlefield: Who Is Winning, Who Is Fading, and Who Has Never Been Found

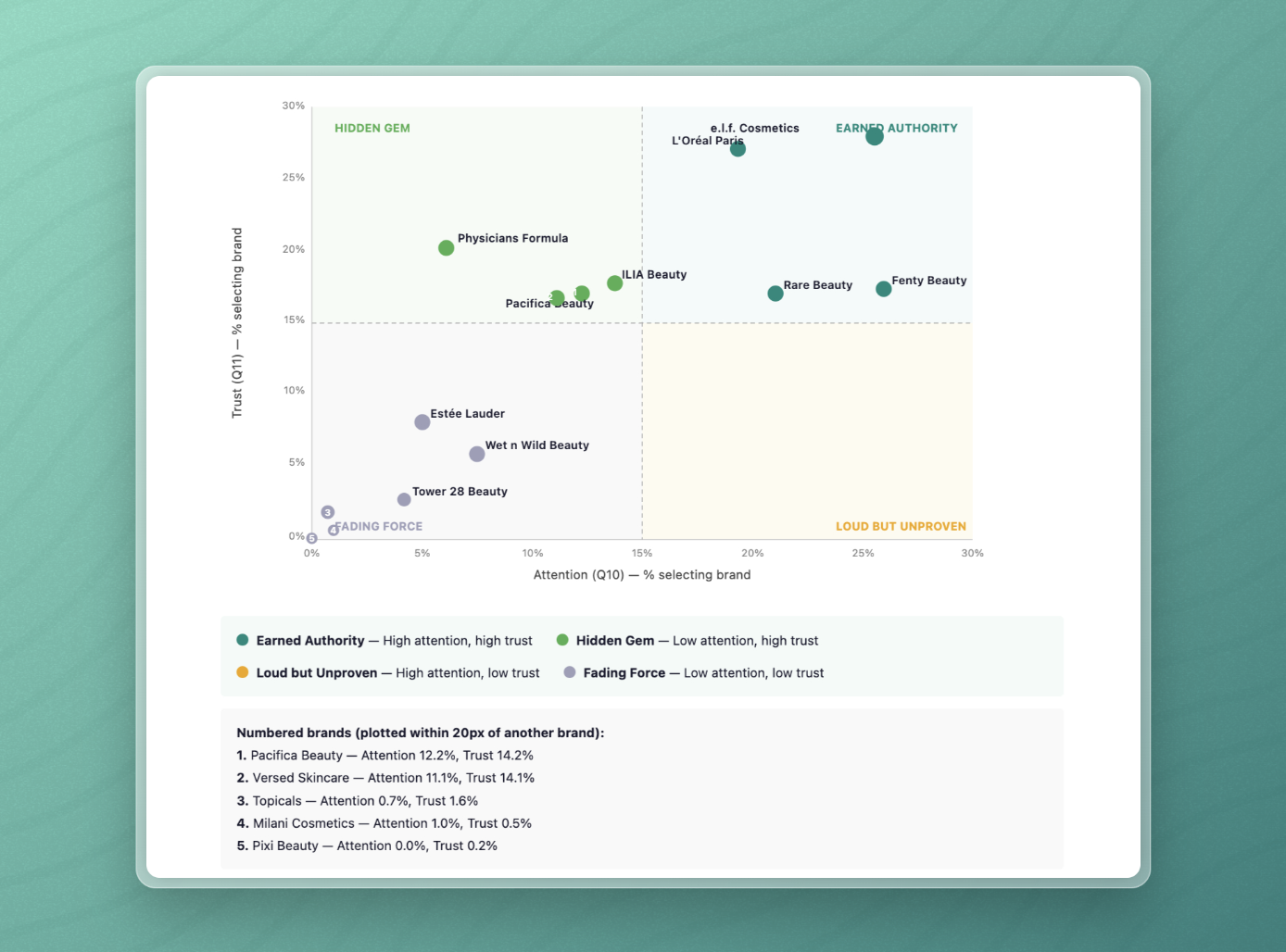

The brand-level data surfaces the most commercially actionable findings in this survey. Across 14 brands — plotted on attention versus trust axes — the map reveals a market bifurcated sharply between brands that have earned their position and brands whose historical advantage is actively eroding.

Earned Authority: The Brands Benefiting From the Trade-Down Moment

e.l.f. Cosmetics leads the entire dataset: 25.5% attention, 23.3% trust, and a brand fatigue rate of just 2.4%. No other brand combines scale and conviction at that ratio. The reason is structural — e.l.f. plays at the price tier consumers are actively moving toward, which means the trade-down moment is not a threat to e.l.f. but a direct tailwind. L'Oréal Paris follows closely at 19.3% attention and 22.6% trust, confirming that accessible credibility is where consumer confidence is concentrating. Rare Beauty (21.0% attention, 14.2% trust) and Fenty Beauty (25.9% attention, 14.4% trust) also qualify for this quadrant — but Fenty leads every brand in the dataset on raw attention while trailing e.l.f. on trust by nearly nine points. In a market where 75% of consumers express price skepticism, attention without trust is a liability that gets more expensive to carry over time.

Hidden Gem: High Conviction, Low Discovery

ILIA Beauty (14.8% trust, 13.7% attention), Pacifica Beauty (14.2% trust, 12.2% attention), and Versed Skincare (14.1% trust, 11.1% attention) post profiles that are nearly identical: high conviction among those who have found them, minimal footprint in the broader cultural conversation. Each has built real credibility without a proportional discovery engine. The most striking case is Physicians Formula, which posts a trust score of 16.8% — third highest of any brand — against an attention score of just 6.1%. That gap represents either a significant distribution and media deficit or proof that the brand has built genuine consumer conviction through channels that generate no noise. The implication is the same either way: Physicians Formula has more earned trust per attention dollar than almost any brand in the category, and whether to activate that asset is a media strategy decision, not a product one.

Fading Force: Heritage Without Credibility

Estée Lauder posts 5.0% attention, 6.8% trust, and a fatigue rate of 46.0% — 265 of 576 respondents selected it as overhyped, overpriced, or outdated. Among active buyers, the fatigue rate rises to 47.5%. Among affluent consumers earning $75,000 and above, it reaches 50.6%. The brand's historical core audience — high-income, category-engaged buyers — is its most active source of rejection. Wet n Wild Beauty (7.5% attention, 4.9% trust) and Tower 28 Beauty (4.2% attention, 2.3% trust) also sit in this quadrant, but the comparison requires care: their fatigue rates are negligible at 0.0% and 1.2% respectively. They are not being rejected. They are simply not being found. That is a different problem — and it has a different solution.

Loud But Unproven - Notably Absent

No brand in this dataset holds high attention with low trust. Every high-attention brand maintains a trust score above the midpoint. In a market where consumer skepticism is running at 75%, the brands winning cultural presence are also winning credibility. The prestige-attention decoupling that has hollowed out brand equity in fashion, spirits, and consumer tech has not yet arrived in beauty with the same force. The window to act before it does is not guaranteed to stay open.

Who Is Actually Trading Down - and Why It Changes the Strategy

Trade-down in beauty is not a distress signal — it is a behavior concentrated among the category's most engaged buyers. Among active buyers, 60.6% have replaced at least one premium product with a cheaper alternative. Among non-buyers, the figure is 4.9% — a 55.7-point gap that confirms the behavior is driven by category knowledge, not category exit.

The income signal sharpens this further. Among lower-income consumers (below $75,000), 56.1% say they are spending less on beauty overall — a volume contraction story driven by budget pressure. Among affluent consumers ($75,000 and above), only 9.7% are cutting spend. But 53.9% of that same affluent segment have already replaced a premium product with a cheaper alternative. These consumers are not budget-constrained. They have concluded — based on ingredient knowledge, peer review, and direct product comparison — that the premium is not justified. They are formula-literate arbitrageurs, not distressed buyers. A brand that diagnoses their behavior as an economic problem and responds with promotions is solving for the wrong variable.

The age signal is worth naming precisely because it is frequently overstated. Trade-down does skew slightly younger — 51.2% of 18–34-year-olds have replaced a premium product versus 42.1% of those 55 and above. But a nine-point gap does not support a generational narrative. Both cohorts cite price and value as the dominant purchase driver above all other influences. This is a category-wide behavior that is modestly more pronounced among younger consumers, not a Gen Z phenomenon that the rest of the market will age out of.

The Strategic Verdict

Ingredient transparency — not heritage, not packaging, not brand narrative — is becoming the threshold criterion for prestige beauty pricing. A brand that cannot make its formula case in plain, verifiable language is exposed. Not eventually. Now, when 50% of consumers say they would walk away from a $65 product the moment they learned a $12 alternative shares its active ingredients.

The addressable opportunity is in the $12–$40 tier, where active substitution is highest and where consumers have demonstrated the greatest openness to conviction through formula legibility rather than prestige signaling. This is where the category's most engaged buyers are making purchase decisions, and where the data shows the highest concentration of switching behavior that a brand with a provable formula could intercept.

e.l.f. Cosmetics is the brand the data identifies as best positioned to capture that moment. Joint-highest trust score at 23.3%, second-highest attention score at 25.5%, a 2.4% fatigue rate, and structural price-tier alignment with exactly where consumer spending is moving. Its full-price conviction score of 10.8% trails ILIA Beauty (20.0%) and L'Oréal Paris (20.1%) — but that gap is not a weakness. e.l.f.'s price point means consumers do not need to persuade themselves it is worth paying full price, because full price is already accessible. The brand has removed the psychological barrier that price justification creates, while retaining the trust scores that brands charging three times more are struggling to match.

The counter-case is Estée Lauder, and it should be read as a warning that extends well beyond one brand. A 46.0% fatigue rate concentrated among active buyers and high-income households — the two segments that historically anchored prestige beauty's pricing power — is not a communications problem. It is evidence that heritage alone no longer functions as a moat in a market where half of all consumers will switch the moment ingredient parity is demonstrated. Any prestige brand whose primary defense is brand equity without a verifiable formula case is positioned identically to Estée Lauder in the data — it simply has not yet accumulated the fatigue score to prove it.

The brands that will hold pricing power in this market are the ones that can prove their formula is worth the premium, not the ones that can narrate it most compellingly. In 2026, those are not the same thing — and the consumer has the tools to check.

Methodology: 576 US adults, nationally representative. Active Buyers (Q5 A+B) N = 432 (75.0%). Non-Buyers (Q5 C) N = 144 (25.0%). Brand matrix analysis covers 14 of 15 brands listed in the survey instrument. Kinship received zero responses across all six brand dimension questions and is excluded from all brand analysis. Pixi Beauty received near-zero responses and is not discussed in brand archetypes. Survey conducted by Standard Insights, April 2026.

Explore the full Beauty & Skincare Dupe Economy report — interactive, filterable, and free to access. Access the report →