The promotional tool most national snack brands are currently relying on to recover private label share is not rebuilding loyalty. It is confirming the trade-down.

According to Standard Insights' May 2026 survey of 554 US adults, nationally representative, 45.5% of consumers will stock up during a name-brand promotion and return to the cheaper option the moment it ends. Discounting is a margin-destroying tactic that temporarily rents volume from consumers who have already decided the premium is not justified.

The full picture is worse. 73.5% of consumers cite price difference as the primary trigger for switching to store brands, not a minority position, nearly three in four. And 38.1% demand clear proof of a meaningful taste or quality difference before they would consider paying more. Vague lifestyle marketing does not move that number. The product has to deliver a verifiable sensory advantage, or the conversation ends before it starts.

This is not a promotional problem. It is a product and positioning problem.

Private Label Snacks vs. National Brands: What the Data Says About Brand Loyalty in 2026

The Purchase Hierarchy Has Flipped

For decades, the assumed decision sequence in packaged snacks ran: taste first, brand familiarity second, price as a tiebreaker at the margin. That sequence justified premium pricing, sustained above-the-line investment, and the belief that brand equity was a durable moat against private label encroachment. Frito-Lay built a $20 billion US snack business on it. So did Mondelēz International.

The PRNewswire data dismantles that assumption directly. Price is now the stated top driver in grocery, not a factor, not a consideration, the top driver, displacing both taste and brand loyalty to get there. That is not a marginal shift in consumer sentiment. It is a structural reordering, and the category pricing logic that national snack brands have operated on for decades was not built to survive it intact.

69% Is a Majority Behavior, Not a Trend

Behavioral data is more reliable than stated preference, and the behavioral data here is unambiguous. Ipsos reports 69% of Americans have increased their private label purchases, a figure that cuts across income levels and demographics in a way that prevents any brand from writing off the threat as someone else's consumer. When a behavior reaches 69% penetration, it has moved well past the early-adopter phase. It is what the majority of American grocery shoppers are doing right now.

The Circana report identifies Gen Z as the primary driver of private label momentum. The strategic implication is not primarily about Gen Z's current share of grocery spending, it is about trajectory. A cohort entering peak spending years having already established private label as a default, rather than a fallback, creates a compounding dynamic that promotional activity alone is unlikely to reverse.

The Trade-Down Is Strategic, Not Desperate

The First Insight data adds a dimension that complicates the straightforward “consumers are squeezed” narrative. Among Gen Z consumers, 59% are trading down on household staples, food and beverages among the most common categories. But the trade-down is not indiscriminate. It is deliberate: consumers are cutting in categories where they believe quality parity exists in order to redirect spending toward categories where they believe it does not. Health and wellness and beauty are where the redirected dollars go. Snacks, for a growing share of consumers, are where the dollars come from.

That framing matters. It means the consumer migrating to private label snacks is not simply choosing cheaper. She is making a quality perception judgment, a conclusion that the name brand does not justify its premium. A snack brand that interprets this as a pricing problem and responds only with promotions may be solving for the wrong variable entirely.

The Diagnosis That Determines the Strategy: Three Forces in Collision

Three forces are now in direct collision in the US packaged snack market, and how they resolve determines what the correct response looks like.

The first is the economic pressure argument. Consumers are squeezed by compounding inflation across housing, energy, and food. Private label growth is the predictable behavioral response. When pressure eases, brand loyalty re-engages and the category resets. This reading counsels patience over repositioning, defend the core, manage trade spend, wait for the cycle.

The second is the quality parity argument. Private label has closed the formulation and packaging gap to a degree that makes the premium unjustifiable for a growing share of consumers. On this reading, economic pressure was the trigger, but quality perception is the mechanism, and once a consumer has discovered that the store-brand version performs comparably to the brand she used to pay more for, the premium may not come back when her wallet does. The Circana report supports this reading: it notes that consumers now report trusting store brands as much as national brands on quality, and that private label quality perception is growing across food and beverage specifically.

The third force makes the question genuinely unresolved: national brands are already responding. The same Circana report notes explicitly that name brands are sharpening pricing, stepping up product innovation, and amplifying digital engagement in direct reaction to private label growth. The category is not static. Brands are moving. The strategic question is whether they are moving toward the right diagnosis, because a CMO who treats a permanent behavioral realignment as a promotional problem will have made one of the more consequential miscalculations of this market cycle.

Existing data characterizes the shift. None of it determines whether consumers who have migrated to private label snacks intend to stay there, or under what conditions they come back.

Standard Insights surveyed 554 US consumers, nationally representative, to find out. We put 15 handpicked brands in front of them, spanning legacy giants with decades of shelf dominance, established challengers navigating the middle ground between name-brand heritage and private label pricing pressure, and lean disruptors that have built audiences by questioning whether the national brand premium was ever justified. The survey was designed around one central diagnostic: are the consumers now buying private label snacks making a permanent decision, or a reversible one, and what would it take to bring them back?

The data identifies which segment is gone, which is recoverable, and what the difference between them actually looks like.

Private Label Snacks Survey: Four Numbers That Define the Brand Loyalty Trap

73.5% of consumers cite price difference as the primary reason for switching to store brands. Not a niche grievance, nearly three in four consumers. Legacy brand equity is irrelevant for the majority.

38.1% demand clear proof of a meaningful taste or quality difference to pay more. Vague lifestyle marketing is failing. The product must deliver a verifiable sensory advantage to command a premium.

45.5% will stock up during a promotion but immediately return to the cheaper option when it ends. Promotions are driving temporary volume, not rebuilding long-term loyalty.

And 24.4% have cut certain snack categories entirely. The threat is not only private label switching, it is total category abandonment as households ruthlessly edit their grocery budgets.

That last figure introduces a dimension absent from the beauty dupe economy finding in Edition 1. In beauty, lapsed buyers were redirecting spend toward premium products they valued more. In snacks, a meaningful share are not redirecting at all. They are simply leaving. There is no redirected spend to capture back with better marketing.

Snack Brand Positioning: Who Is Winning, Who Is Fading, and Who Has Already Lost

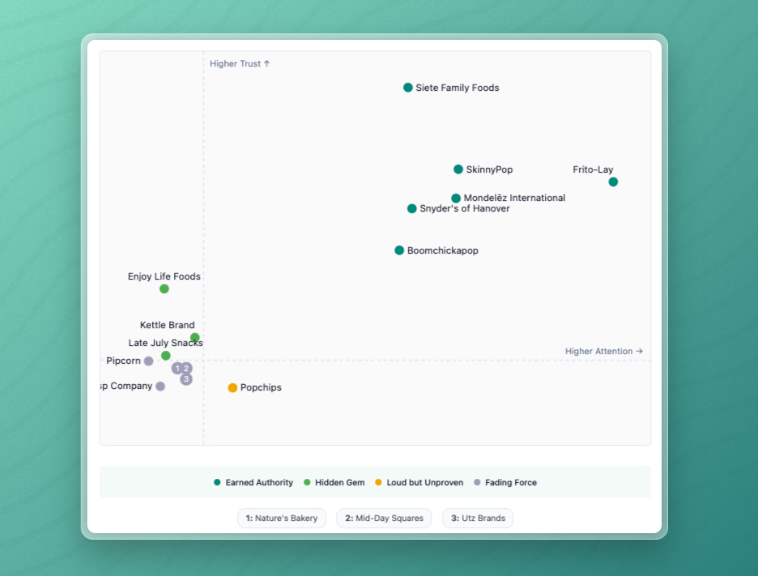

The brand matrix plots 15 handpicked snack brands on attention versus trust, the same two axes used in Edition 1, to surface where category conviction is concentrating and where scale is quietly becoming a liability.

Earned Authority: Structural Insulation in a Commoditized Market

Siete Family Foods dominates this quadrant with category-leading trust (254) on highly efficient attention (179).

Editorial note: Siete Family Foods was acquired by PepsiCo in 2023. Frito-Lay, a PepsiCo division, is listed as a Legacy Giant in this survey instrument. Consumer perception data for Siete reflects responses collected prior to any material change in brand positioning following the acquisition. Both brands are included independently based on consumer-facing identity.

Their positioning is built on cultural identity and ingredient specificity, a combination that translates directly into pricing power because the private label alternative cannot replicate either. A consumer who buys Siete is not buying a grain-free tortilla chip. She is buying a brand that reflects something about who she is, which means the purchase decision is not a price comparison. Frito-Lay also sits in this quadrant on the strength of its attention score, but its fatigue rate (289) signals the kind of accumulated consumer resistance that appears beneath the volume numbers before it appears in the revenue line. SkinnyPop also qualifies, holding a trust position that its better-for-you positioning actively earns rather than assumes.

Hidden Gem: The Defensive Moat That Needs No Campaign

Enjoy Life Foods operates with minimal attention (37) but disproportionate loyalty (111 trust). A brand built on specific dietary needs does not need to win the attention game. Its audience is not shopping by scroll, they are shopping by necessity, which means Enjoy Life operates with a highly defensive moat that requires no expensive mass-market campaign to maintain. This is what category-specific identity looks like when it functions correctly.

Loud But Unproven: Reach Without Conviction

Popchips sits alone here, moderate attention (77) that fails to convert into trust (40). Marketing is visible. Conviction is not. A brand in this position is paying for reach without earning purchase intent, which makes it the most exposed to private label substitution of any brand in the dataset. When a consumer can swap the product without feeling they have compromised on anything, awareness alone gives them no reason not to.

Fading Force: Same Quadrant, Different Problems

Utz Brands and Mid-Day Squares both cluster in the bottom left, struggling to break 55 on either metric, but the comparison requires care. For Utz, a legacy brand with broad distribution, this signals a dangerous slide into commoditization: the kind of brand consumers reach for when nothing else is available, not because they chose it. For Mid-Day Squares, an emerging brand still building its US presence, the same coordinates represent a different problem, the rising cost of acquiring initial consumer trust in a market where skepticism is the default. Same quadrant, structurally different situations, completely different solutions.

Nature's Bakery, Snyder's of Hanover, Mondelēz International, Kettle Brand, Late July Snacks, and Boomchickapop cluster in the middle range, the brands navigating the premium middle ground where private label pressure is most acute and where the absence of a defensible positioning argument is most commercially dangerous.

Private Label Trade-Down: Who Is Gone, Who Is Recoverable, and Why Promotions Are Making It Worse

Trade-down in snacks is not a uniform behavior, and the gap between Active Buyers and Non-Buyers reveals why the standard recovery playbook is misfiring.

When asked how their grocery shopping has changed, 68% of Non-Buyers report cutting snack categories entirely, compared to just 20% of Active Buyers. A 48-point gap that confirms lapsed buyers are not switching to competitors or trading down to private label. They are leaving the aisle altogether because the price-to-value equation has broken down past the point of substitution. There is no redirected spend to intercept with a better promotional offer.

The promotional loyalty gap tells the next part of the story. Following a price promotion, 35% of Active Buyers will stay with the name brand, but only 12% of Non-Buyers will do the same. A 23-point gap that means promotions are effectively rewarding consumers who were already purchasing, while acting as a temporary rental of share for those who have traded down. A discount that fails to convert lapsed buyers is a margin cost with no recovery attached to it.

The sensory justification gap is the most actionable finding in the report. 41% of Active Buyers require clear proof of a taste or quality difference to pay a premium, compared to 22% of Non-Buyers. Active buyers are willing to trade up, but only when the product delivers a verifiable advantage over the private label alternative. The path back to this segment is not above-the-line spend. It is product proof delivered at the moment of decision.

Snack Brand Loyalty by Age and Income: The Signals National Brands Are Missing

38% of consumers aged 18-34 cite values alignment, sustainability, clean ingredients, modern identity, as the primary reason they would pay more for a name brand, compared to just 14% of those 55 and older. Clean ingredients are not a differentiator for younger cohorts. They are table stakes for consideration. A national snack brand targeting both age groups with a single value proposition built around taste or convenience is failing to give younger buyers a reason to engage and over-serving older buyers with messaging they do not need.

The income signal is starker. 88% of households earning under $50,000 switched to store brands because of price difference, versus 62% of households earning $75,000 or more. The cost-of-living squeeze has effectively eliminated brand loyalty at the lower income tier, turning legacy snack brands into a pure commodity for that segment. The strategic opportunity, as in Edition 1's affluent consumer finding, sits in the higher-income bracket, but the barrier is not aspiration. It is verifiable quality. An affluent consumer who has concluded the premium is not justified will not be moved by brand heritage or a loyalty program. They need a product argument.

Private Label Snacks: The Strategic Verdict for National Brand CMOs

Price promotions are masking a structural decline in category loyalty. With 45.5% of consumers confirming they will return to private label the moment a promotional period ends, discounting is functioning as a volume-smoothing mechanism, not a loyalty-rebuilding one. A CMO who reads a volume spike during a promotional window as evidence of recovering brand preference is misreading the signal. The volume was rented. The loyalty was not restored.

Siete Family Foods has demonstrated what structural insulation looks like in a commoditized environment. Category-leading trust (254) paired with the highest modern identity score in the dataset (277) has produced pricing power that private label cannot erode, because the purchase is not a product decision, it is an identity decision. Cultural relevance is not a niche play in this market. It is currently the most durable moat available, and the data shows it functioning exactly as intended.

The warning that extends across the category sits with Frito-Lay and Mondelēz. Both command massive attention. Both carry extreme fatigue rates, 289 and 283 respectively. Their scale is generating reach without conviction, which is the signature position of a brand that is actively giving consumers permission to look for alternatives. The parallel to Estée Lauder in Edition 1 is direct: attention without trust, in a market defined by price skepticism, compounds into structural share loss. The volume numbers have not yet reflected what the sentiment data is already showing.

The path back from private label is not promotional. It requires one of three things: sensory proof that the product delivers a verifiable advantage the store brand cannot match, values alignment that makes the private label alternative feel like a genuine compromise rather than a rational substitution, or category-specific identity that removes the brand from price comparison entirely. Any brand that cannot make one of those three cases at the product level is relying on a marketing argument in a market that has stopped listening to marketing arguments.

In 2026, the consumer is checking the shelf every week. A coupon is not an answer to the question she is actually asking.

Methodology: 554 US adults, nationally representative by age, gender, and region. Active Buyers (purchased packaged snacks in the last 6 months) N=507 (92%). Non-Buyers (opted out of snack purchases recently) N=47 (8%). Brand matrix analysis covers 12 of 15 brands listed in the survey instrument, three brands were excluded from all brand analysis due to category misclassification in the survey instrument and received no usable responses within this study's scope. All percentages calculated as a share of total N (554) unless otherwise stated. Active Buyer and Non-Buyer sub-group percentages calculated as a share of each respective sub-group. Note: Siete Family Foods was acquired by PepsiCo in 2023. Frito-Lay, a PepsiCo division, is listed separately in this survey as a Legacy Giant. Consumer perception data for both brands reflects independent consumer-facing identity at the time of fieldwork. Survey conducted by Standard Insights, May 2026.