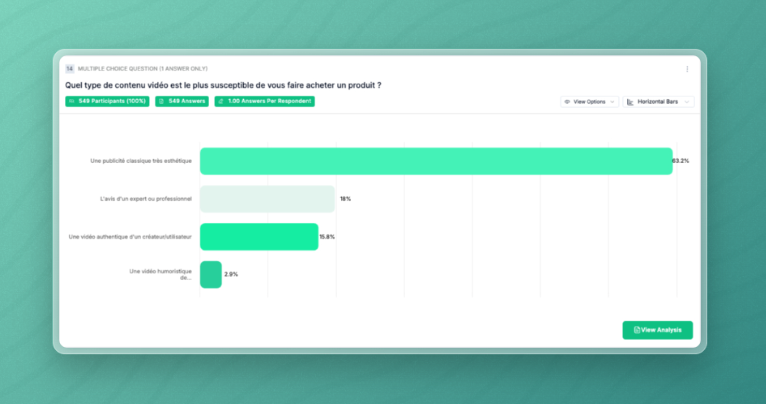

63% of French consumers require traditional aesthetic advertising, not creator video, not UGC, not social content, to trigger a purchase. In a market where creator content has dominated the acquisition conversation for five years, that number lands hard. Brand-quality visual production is not a legacy preference among older consumers. It is the majority conversion mechanism across the French market in 2026.

The structural tension underneath that finding is what makes it commercially significant. Social media is the dominant brand discovery channel: 214 respondents in the Consumer Brand Discovery France 2026 study cite it as their preferred channel for finding new brands, ahead of traditional advertising at 193. Discovery is running on social. Conversion is not. Those are different behavioral moments, and most brands are currently optimizing for one while neglecting the other.

Which channels are winning which part of the funnel, which consumer segments behave differently, and what that means for acquisition investment in France: that is what the data resolves.

Social Media Dominates Brand Discovery in France, But Not Evenly

The platform fragmentation by age is the most commercially actionable finding in the discovery layer, and it argues directly against any single-platform acquisition strategy targeting broad French audiences.

Facebook dominates among consumers 35 and older, cited by 58% of 35-54-year-olds and 86% of those 55 and above as their primary discovery platform. TikTok dominates among 18-24-year-olds at 46%, with Instagram at 36%. A brand running discovery spend exclusively on TikTok and Instagram is invisible to the majority of French consumers over 35. A brand running exclusively on Facebook is absent from the platform where younger cohorts are actively being introduced to new brands. These are not adjacent audiences. They are operating on entirely separate discovery architectures, and the data makes that impossible to paper over with a broad demographic target.

The discovery frequency gap compounds the challenge. 71% of the engaged consumer group, those already primed to purchase via social influence, discover new brands through social more than once per week. Among the non-engaged group, that figure drops to 23%. The algorithm rewards consumers who are already open to brand discovery, surfacing them more brand content and reinforcing the behavior. This creates a two-speed market: digitally active consumers who encounter brands constantly, and traditionally oriented consumers who are structurally underserved by social-first approaches.

Television retains structural weight at the top of the funnel that social-first strategies have been too quick to abandon. 246 respondents, out of a 549-person nationally representative sample, report discovering no new brand via social media in the last three months. These consumers are still entering brand awareness through traditional media. Any acquisition strategy that has fully withdrawn from broadcast is ceding that audience to competitors who have not.

Why the Channel That Finds the Customer Is Not the Channel That Converts Them

Standard Insights surveyed 549 French consumers using a nationally representative survey methodology on discovery behavior, purchase triggers, and format preferences. The conversion findings are where the data becomes most commercially uncomfortable for brands that have reallocated creative budgets toward UGC and creator-led content.

The 63% traditional advertising preference is not confined to older cohorts. It is a cross-demographic majority position. Authentic creator video is preferred by 87 respondents across the full sample, a meaningful segment, but not a majority. For most French consumers, the moment of purchase permission is not unlocked by a creator recommendation or a first-person unboxing video. It is unlocked by brand-controlled visual production that signals the brand takes itself seriously enough to invest in how it is presented.

The age breakdown on video format preference is the most counterintuitive finding in the study and should be named directly in any media planning conversation. Among 18-24-year-olds, 48% prefer authentic creator video, but 32% prefer traditional aesthetic advertising. The creator-first narrative is real for this cohort, but it is not total. Among 35-54-year-olds, 64% prefer traditional aesthetic advertising and only 18% prefer creator video. Among those 55 and above, 79% prefer traditional advertising and just 6% prefer creator content. The authenticity-beats-polish argument is a minority preference even among the youngest French consumers, and a strongly minority preference among every cohort above them. Brands targeting the 35-plus French consumer with creator-led creative as a primary conversion format are not meeting a preference. They are imposing one.

The word-of-mouth signal sharpens the conversion picture further. Among non-influencer buyers, the 59% of respondents not primed to purchase through social channels, 81% cite word-of-mouth as their final decision mechanism. Among influencer buyers, 58% cite social media. That 29-point gap is not a platform gap. It is a trust gap. For the majority of French consumers, the transaction is closed by a peer recommendation, not a paid channel. A brand with no organic recommendation or community strategy is relying entirely on paid acquisition to close a sale that peer conversation closes more reliably and at no marginal cost.

The French Consumer Is Not One Audience, and the Data Shows Where the Fault Lines Are

The gender signal on word-of-mouth has direct budget allocation implications. Women are significantly more likely to cite word-of-mouth as a final decision channel than men, 54% versus 33%, a 21-point gap. For brands whose primary French target is female, a paid social strategy without a recommendation layer is structurally incomplete. The conversion mechanism the audience actually uses is not being funded.

The engagement gap between influencer buyers and non-buyers confirms that social reach and social conversion operate on different logic. The 62-point gap in social purchase probability, 94% among influencer buyers versus 22% among non-buyers, is not primarily a content quality problem or a targeting failure. It reflects a genuine behavioral divide between consumers who are already open to social-driven purchase decisions and those who are not. The algorithm amplifies that divide by surfacing more brand content to the already engaged. For brands targeting the non-engaged 59%, social spend generates awareness that is not converting, because the conversion mechanism for that segment runs through different channels entirely.

What French Brand Marketers Need to Rethink Before the Next Campaign Brief

The data does not argue against social media investment. It argues against treating social media as a full-funnel channel. Discovery investment, TikTok and Instagram for 18-24-year-olds, Facebook for those 35 and above, and conversion investment, traditional aesthetic advertising, word-of-mouth activation, community-driven recommendation, are different budget lines serving different behavioral moments. A brand that has collapsed those into a single social-first strategy has built a discovery engine with no conversion mechanism attached.

The 63% traditional advertising preference is a trust signal, not a nostalgia signal. Brand-quality visual production communicates that a brand is worth taking seriously at the moment of purchase. Creator video communicates discovery-friendly accessibility. These are not interchangeable messages, and they are not interchangeable at the same funnel stage. The brands that are performing both functions with a single creative format, usually creator-led because it is cheaper to produce, are getting one of those jobs done at the expense of the other.

The French market in 2026 is running a bifurcated purchase journey that most acquisition strategies are not built for. The same consumer who finds a brand on TikTok is likely to complete the purchase only after encountering brand-quality creative or a peer recommendation, not because the TikTok content failed, but because discovery and conversion are sequential jobs requiring different tools. The brands that will hold conversion efficiency in this market are the ones that fund both halves of that process, not the ones that measure only the half the algorithm surfaces first.

Methodology: 549 French consumers, nationally representative. Influencer buyers (Acheteurs via Influence): N=224 (41%). Non-influencer buyers (Non-acheteurs via influence): N=325 (59%). Full methodology and persona breakdown available in the Consumer Brand Discovery France 2026 report.